ARTICLE

How PSPs fight IBAN discrimination

28 February 2023

In 1997, the European Committee for Banking Standards (ECBS) introduced the International Bank Account Number (IBAN) with the goal of standardising bank account identification standards throughout Europe. Prior to this, local identification standards were causing complexity for payment flows within Europe. In 2009, the first Payment Services Directive (PSD1) was passed, allowing payment service providers (PSPs) regulated in any European country to operate across all European markets through passporting.

However, despite these efforts towards standardisation and simplification of processes, there remain significant operational complexities that fintech companies must navigate when expanding across Europe. One such issue is IBAN discrimination.

What is IBAN discrimination?

IBANs (for international bank account numbers) are used to normalise account numbers across more than 80 countries, including the 36 countries of SEPA.

IBANs are the only account numbers usable for SEPA payments.

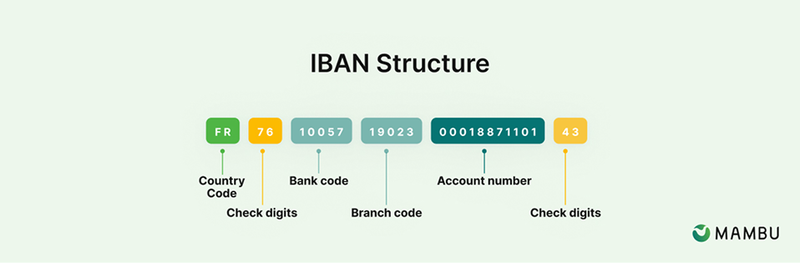

IBANs always start with a country code and include a bank code, which is the bank code of the financial institution holding the account linked to an IBAN.

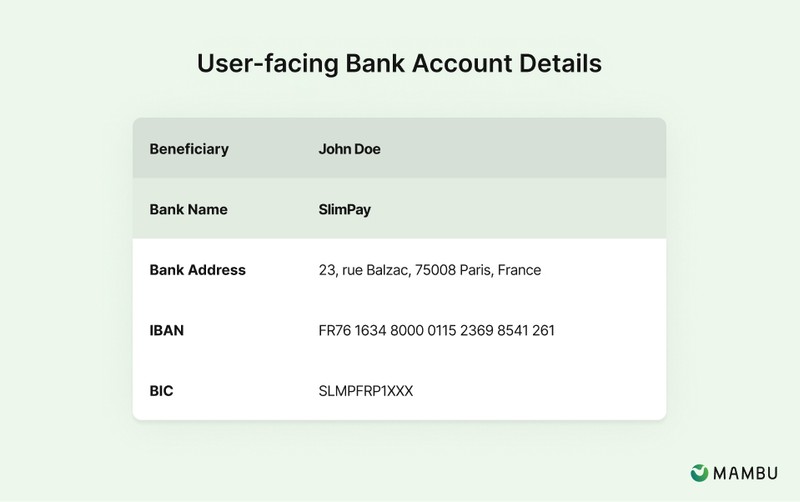

In the case of SEPA payments, end customers will see BICs and IBANs when sending SEPA payments. They will have to fill in the IBAN of the payment’s beneficiary. Financial institutions will show the name of the financial institution holding the account corresponding to the IBAN to their end customers. Examples include when the end customer needs to top up a digital wallet via SEPA payment, pay a bill, or send money to a friend.

IBAN discrimination is a form of financial inequity that has been affecting customers across the European Union since the beginning of the 2010s. It occurs when companies or employers refuse to accept an IBAN for euro payments due to its country code, which can lead to customers being unable to access certain services. This practice was made illegal in 2014. However, fintech companies building across Europe are still experiencing issues resulting from it. For UK fintech companies specifically, Brexit has triggered renewed concerns about this problem for GB IBANs.

As a way of fighting back against IBAN discrimination, fintech scale-ups such as Wise have launched initiatives like AcceptMyIBAN, which tracks instances of IBAN discrimination and educates customers on how to manage any issues they may encounter. Research has shown that France, Germany, and Spain are currently the biggest offenders when it comes to this type of financial inequality. Other examples of reactions from fintech companies have been Revolut Ireland, which decided to migrate its Lithuanian IBANs to local Irish IBANs and Starling Bank communicating to its customers about how to deal with these situations.

Other strategies for addressing the issue include creating awareness about the prevalence and consequences of IBAN discrimination within the EU as well as pressuring large companies who engage in this practice either knowingly or unknowingly. This could be done with campaigns aimed at raising public concern over the issue and lobbying governments for stronger measures that would prevent further discrimination from taking place in the future. In addition, organisations should provide better customer service and advice on how consumers can protect themselves from this financial injustice.

Mambu Payments’ IBAN survey results

To understand which components of IBANs and bank coordinates influenced consumers when selecting financial services, we ran a survey on 200 French consumers via Survey Monkey. France was chosen as, according to Acceptmyiban.org, it is the country with the highest reported occurrences of IBAN discrimination.

In the first question, we asked consumers how likely they were to trust and use financial services that required them to send payments to 6 different bank coordinates, with the following varying characteristics:

- BIC

- Beneficiary

- Bank name

- Bank address

- According IBAN

The results are striking: the most significant criterion is the localisation of the bank coordinates, and therefore IBAN.

Indeed, surveyed French consumers were on average 83% more likely to use financial services using a local, French IBAN compared to other alternatives.

In more detail, they were 45% more likely to use services using French IBANs than German IBANs, and 110% more likely to use services using French IBANs than Lithuania or Gibraltar IBANs.

We also surveyed French consumers on their IBAN discrimination experience.

25% declared they experienced IBAN discrimination when using a foreign IBAN, and 29% when using an IBAN of an account that was not in their name.

IBANs and PSPs: at the core of the digital wallet

At the core of many PSP offerings are the ability to open and use wallets to receive and send payments. These wallets leverage dedicated IBANs (corresponding virtual accounts or actual accounts) to track customer balances as they top up and payout.

For customers, the PSP linked to an IBAN matters. When sending money to a digital wallet, consumers are twice as likely to trust an IBAN from their own country than from a foreign country. The PSP linked to an IBAN depends on the PSP’s bank identifier code (or BIC) used to identify PSPs across the SEPA zone.

There are three main ways that PSPs can issue IBANs for their customers’ accounts, with different implications for their branding:

- Become a SEPA participant and issue their own IBANs to their customers. In this scenario, the IBANs are linked to the PSP’s name as the financial institution holding the account. The PSP needs to register with the EPC and the SEPA clearing and settlement mechanisms as well as be able to send and receive SEPA payments through its sponsor bank, using a payment operations platform like Mambu Payments.

- Virtual IBANs from a partner bank. Banks in the EU are increasingly offering a virtual IBAN service alongside their settlement and safeguarded account offering for PSPs. In this scenario, the IBANs are linked to the name of the partner bank.

- Virtual IBAN from another fintech company. In this scenario, the fintech company uses IBANs issued by another fintech company in their name to share with its customers. In this scenario, the IBAN is linked to the name of the partner fintech company.

Strategies to mitigate IBAN discrimination

While there is no silver bullet to root out IBAN discrimination completely, there are ways for PSPs to mitigate its impact through local IBAN strategies.

Having your own local IBANs as a SEPA participant

In order to take advantage of local IBANs, PSP companies need to open subsidiaries or branches in the relevant countries, apply for a bank code from the local regulator, and register a new BIC with Swift. Once this process is complete, PSPs are able to generate their own local IBANs as SEPA participants that can be used throughout Europe.

Despite the potential benefits of this method, it does come with certain drawbacks – namely increased regulatory supervision by local authorities and associated costs of this regulatory oversight.

Leveraging virtual IBANs through a network of local partner banks and accounts

If applying for a local bank code is too much work, another option is leveraging bank virtual IBANs through a network of local accounts across Europe. This approach involves opening multiple accounts at banks in different countries and using virtual IBANs associated with accounts. Any payments received through these virtual IBANs can then be securely held in affiliated bank accounts subject to applicable regulations governing each country. France, Germany, and Spain are the three countries that have been identified as having the highest degree of IBAN discrimination, so it can be beneficial for fintech companies to build with local IBANs from those markets.

The complexity of this method lies mainly in orchestrating the banking operations without having to register for a local bank code. It also doesn’t allow for the PSP to have IBAN branded in their name.

Leveraging the flexibility of bank aggregation

At Mambu Payments, we believe that being a SEPA participant and having partner banks across Europe are key for the lasting success of fintech companies.

By providing bank aggregation and SEPA participation into a single API, Mambu Payments’ platform enables banking and strategy teams to make the right strategic decisions for their business without having to factor in the product and technical opportunity costs of building new bank integrations. Mambu Payments also makes it easy to set up the cross-bank orchestration required to move funds between bank accounts to support payment operations and regulatory requirements.

© Mambu 2026