ARTICLE

The State of Instant Payments in European countries

Instant payments gradually emerged around the world at the beginning of the 2000s. In Europe, they first appeared in the United Kingdom in 2008, followed by Sweden (2012), Poland (2012) and Denmark (2014). A unified scheme, SEPA Instant Credit Transfer (SCT Instant), only emerged in 2017.

Interestingly, each local system adopted different approaches to design and implementation and kept some local specificities.

What are the common patterns across European countries’ real-time payment solutions?

Instant payments are aimed at being processed and cleared 24/7/365. But there are a few limitations in some local systems.

Within seconds (usually 5 to 10), funds are made accessible to the beneficiary, and the funds deposited to their account are irreversible and immediately available to the account owner. A standard message is provided to the payer if the transaction is declined.

Here again, some local limitations may exist. In the UK, faster payments might take up to two hours to reach the beneficiary’s account.

Even though the need for instant payments has been increasing over the past ten years, traditional payment infrastructures have not been able to keep up with demand. Credit transfers were typically cleared and paid within one weekday (t+1) until a few years ago. Thus even the advent of intraday clearing represented a significant advancement.

How do settlement and clearing mechanisms work in European real-time transactions

Clearing and settlement mechanisms are at the core of payment systems. And no evolution of speed of payments would be possible without evolutions on the traditional once-a-day clearing and settlement.

In order to ensure real-time payments, three systems and philosophies have been designed in Europe.

Real-time settlement systems

In this system, the settlement of each payment is performed in real-time on an ongoing basis. The immediate and final settlement of the payment occurs simultaneously with the participants' exchange of payment orders.

Consequently, participants in the system will need a high volume of liquidity and implement specific security measures on their dedicated accounts.

Deferred net settlement systems

This second system is the most frequently used across the EU.

Payment orders and execution of payments are done during dedicated clearing cycles. Settlement of payments occurs at a different time within settlement sessions: a settlement agent – usually the Central Bank – credits and debits each participant’s account to the system.

The main advantage is that you don’t need such a high volume of liquidity as in the real-time settlement system. Orders do not have to be settled one by one and covered by funds.

On the minus side, higher security measures are necessary in case of issues to guarantee payment execution.

This system has been adopted in the UK for its faster payment service.

Prefunding, deposit model

This system implies that each participant has a defined limit of transactions, covered by funds earlier deposited on a dedicated account.

How the EU aims at unifying standards and schemes in the EU?

With each country adopting its own vision of how to implement local instant payments, cross-border operations were getting increasingly complex.

No cross-border operations mean no single market. Thus, the European Payments Council (EPC) prepared the harmonised rulebook for SEPA instant payment process flows and data contents in 2016, revised in 2017 and 2018. In November 2017, the EPC Sepa Credit Transfer (SCT) instant scheme became operational.

The scheme requests to adopt a few features, including:

- A maximum duration of ten seconds before the beneficiary’s PSP provider notifies the payer’s PSP of the success or failure of the payment.

- A maximum amount of 100,000 euros per transaction

- The services must be available 24/7/365

- The transactions shall be made in euros, but accounts can be in any currency

How the EU aims at unifying standards and schemes in the EU?

With each country adopting its own vision of how to implement local instant payments, cross-border operations were getting increasingly complex.

No cross-border operations mean no single market. Thus, the European Payments Council (EPC) prepared the harmonised rulebook for SEPA instant payment process flows and data contents in 2016, revised in 2017 and 2018. In November 2017, the EPC Sepa Credit Transfer (SCT) instant scheme became operational.

The scheme requests to adopt a few features, including:

- A maximum duration of ten seconds before the beneficiary’s PSP provider notifies the payer’s PSP of the success or failure of the payment.

- A maximum amount of 100,000 euros per transaction

- The services must be available 24/7/365

- The transactions shall be made in euros, but accounts can be in any currency

What are the benefits of local real-time payments in European countries?

The core of the modern economy relies on efficient and secure payments. Businesses cannot ignore the rising demand for faster transactions in a customer-centric world. These expectations are true both within the B2B and the B2C world, for businesses and merchants alike.

The need for real-time payments is global: all continents are looking for ways to replace the ease of cash payments with digital solutions.

From a customer perspective, real-time transactions mean:

- Convenience

- Easier liquidity management

- In some cases, faster deliveries.

From a bank point of view, real-time payments:

- Directly compete with cash operations, which still account for between 5 and 10 per cent of their total operating costs

- Allow them to provide some more paid alternative options to their customers.

What are the main drawbacks regarding real-time payments?

From a consumer point of view, some potential additional fees may appear because of this system. Perhaps more crucially for the customers, in countries where the adoption of the new system is not large enough, it can be challenging to understand where instant payments can be used.

For the banks, single real-time transactions are limited in value and maintenance costs may be high.

Fraud is also an essential factor to consider. Faster payments might mean faster fraud in some cases.

Also worth mentioning is the potential high competition for the service operators. Additionally, more traditional mobile phone payment solutions exist in countries where instant payments are accessible through mobile applications, such as Google Pay or Apple Pay.

An overview of European real-time payment systems, country by country

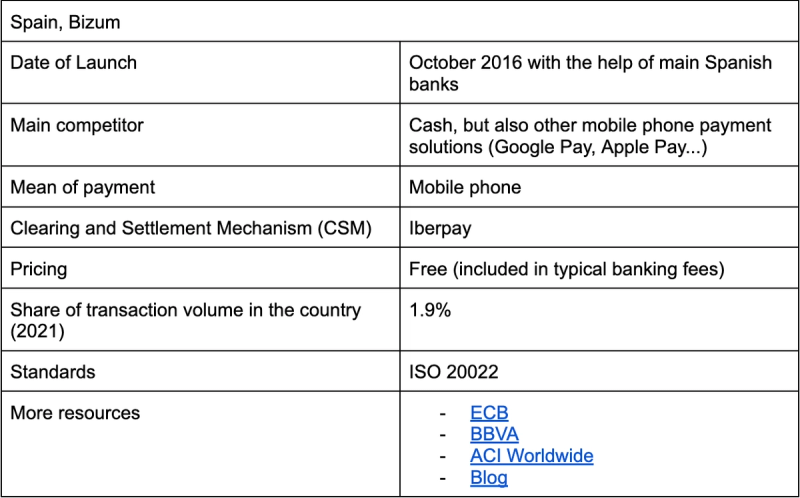

Spain, Bizum

Bizum is an instant payment service that lets users transfer money from their account to another person’s account without needing to know their account number. The transfer is made through a mobile phone.

Bizum is built according to the SCT Inst standard. In short, it is an informational layer leveraging the new SEPA real-time payment standard.

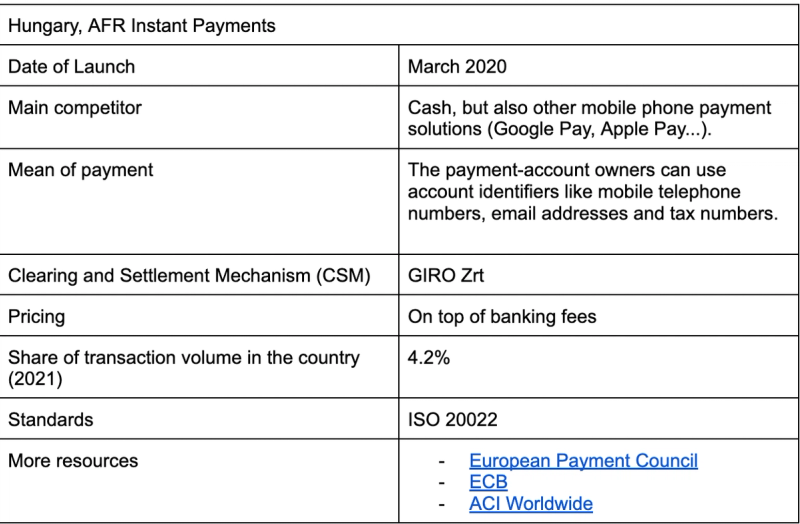

Hungary, AFR Instant Payments

The Hungarian Instant Credit transfer scheme (AFR Instant Payments) was successfully launched on March 2nd 2020.

Following a three-month public consultation in 2016, the central bank decided to implement the scheme and began setting up the national project in collaboration with the clearing house GIRO Zrt, the operator of the current retail payment systems, and 35 payment service providers (PSPs) on an obligatory basis.

Despite Hungary’s absence from the eurozone, the local instant payment system was designed to be implemented in a way that complies with standardised European standards.

Since numerous Hungarian banks based their instant payment projects on those of their international parent banks, and IT developers were more experienced with European schemes, this was also seen as being crucial for lowering the development costs of payment service providers.

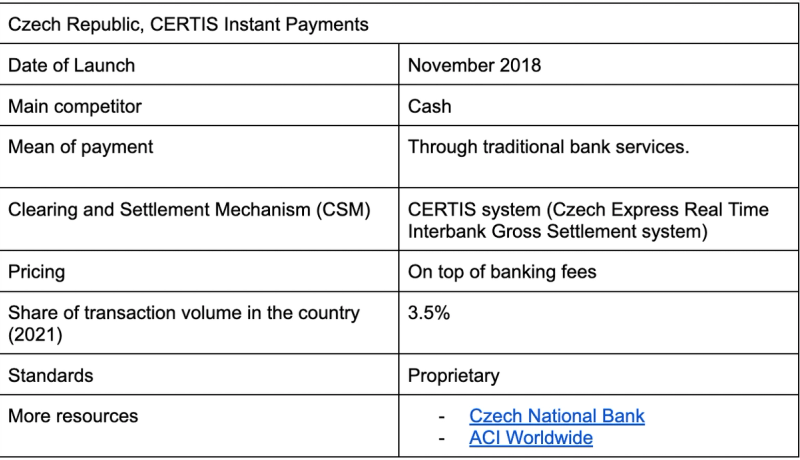

Czech Republic, CERTIS Instant Payments

Czech’s CERTIS Instant Payments was launched in November 2018. The state of payments in the country is slightly different from what is found elsewhere in the EU. In 2017, the Czech Republic had the largest number of credit transfers per capita (171.8) in Europe (vs 62.6 on average).

Instant payments enable customers of Czech banks to make one-off credit transfers in Czech koruna (CZK) in seconds. A bank must join the instant payment scheme and be a CERTIS participant in order to be able to provide this service to consumers. Since participation in the program is optional, not all CERTIS participants offer their clients instant payments service.

© Mambu 2026